With Shared Ownership Week approaching in September, now is the ideal time to explore how using this scheme could be a helpful stepping stone to owning your own home, while also considering its potential drawbacks.

Shared ownership is designed to make the path to homeownership more accessible, as you buy a share of a property and pay rent on the rest. This can be particularly useful for first-time buyers.

A key part of this is “staircasing”, a common process in shared ownership that could eventually lead to you owning your home outright.

This said, some aspects of shared ownership may be less appealing than buying an entire home in the traditional way.

Here’s what you need to know about shared ownership, staircasing, and some important factors to consider.

Shared ownership is a government-backed scheme that allows you to buy a share of a property

When you purchase a home through a shared ownership scheme, you will typically buy between 25% to 75% of the property and pay rent on the remaining portion.

Opting for a shared ownership home could significantly reduce the deposit you need to buy a house outright, making it an attractive option for those who might struggle to save a large deposit or meet the affordability criteria for a traditional mortgage.

When lenders consider your affordability, they’re looking at your income, expenses, and existing debts. They do this to ensure you can comfortably afford the monthly mortgage payments.

They will also factor in your monthly rent, so it’s important to understand how this could affect your monthly finances.

How your rent will work

The rent limit is 3% of the value of the share the landlord owns. Though your rent may fluctuate, there are rules in place that prevent it from increasing too much.

According to the government, if you signed your lease on or after 12 October 2023, your landlord could increase your rent by one of the following each year:

- The Retail Prices Index (RPI) plus up to 0.5%

- The Consumer Prices Index (CPI) plus 1%.

This means that if the RPI or CPI increased dramatically over a year, you could see a marked increase to your rent.

How your mortgage will work

Since lenders use your affordability (a calculation based off your income and expenses), you may be concerned that lenders won’t consider you for a full mortgage, even if you could afford it.

Shared ownership could help with your affordability, particularly if you consider the average cost of buying a house in the UK, which can be a barrier to homeownership for many in the UK.

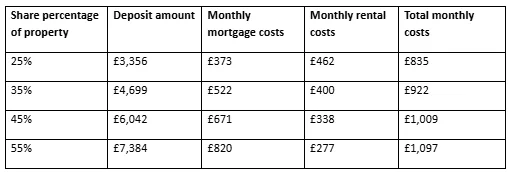

According to December 2024 report from Nationwide, the average property price in the UK was £268,518. Using this as a baseline, we can estimate how much your monthly costs could be for your mortgage, though it’s important to keep in mind that house prices tend to increase each month by a small amount.

For this example, we’ll use a 5% deposit, a repayment mortgage with a term of 25 years, and a 5% interest rate.

Source: Plumlife Homes

As you can see, the higher your share of the property, the more your total monthly costs could be. However, you would also own more of your home and pay less rent. Depending on your circumstances, you might find it worthwhile to increase your deposit to purchase a larger share.

Importantly, if you have a fixed-rate mortgage, your monthly mortgage payments will remain the same until you need to remortgage. If you have a tracker- or variable-rate mortgage, your monthly payments could fluctuate if interest rates change.

Staircasing offers a way to achieve full ownership of your home

Staircasing is the process of buying additional shares in your shared ownership property, gradually increasing the percentage of your home that you own. As you staircase, the amount of rent you pay decreases, which brings you closer to owning 100% of the property.

Here’s how it typically works:

- You will usually buy additional shares in percentage increments. The amount you can buy each time will be determined by the Housing Association. Each time you staircase, the new share’s value is based on the property’s current market value.

- To purchase new shares, you’ll likely need to remortgage or secure additional financing. Be sure to factor in the fees involved, such as valuation fees, legal costs, and mortgage arrangement fees. A mortgage adviser can help you navigate this process.

The ultimate goal for many with a shared ownership home is to reach 100% ownership at some point, as this can provide long-term financial security and freedom.

However, while shared ownership can offer significant benefits, it’s essential to be aware of the potential drawbacks.

Drawbacks to consider include uncapped service charges and a lack of communication

A June 2025 report from the BBC highlights a rising number of complaints about the shared ownership scheme. It indicated that shared ownership complaints soared by almost 400% between 2020 and 2024, with the Housing Ombudsman receiving 1,564 complaints in 2024, compared to 324 in 2020.

Common complaints often relate to:

- Repairs and maintenance costs. Shared owners are typically responsible for all repairs and maintenance on the home, even if they only own a small share. This can lead to unexpected costs that would otherwise be covered by the landlord if they were renting.

- Service charges. While rent is capped based on inflation, uncapped service charges can increase monthly expenses significantly, with the BBC also reporting that a shared ownership homeowner had seen a £200 monthly increase in her service charges.

- Complexity and communication issues. With so many different parties involved, including the owner, housing association, freeholder, and managing agent, communication breakdowns can arise and lead to difficulties in resolving issues.

- Selling the property. There can often be complications and delays when selling a shared ownership property, with Housing Associations usually having the first right to find a buyer.

Ultimately, you may experience a mismatch between your expectations of shared ownership compared to how the scheme works in practice, but doing your research and working with an expert can help minimise the risk of this happening.

Working with an adviser can make it easier to find your dream home

Shared ownership can be an excellent way to achieve homeownership, offering a flexible route onto the property ladder. By understanding how staircasing works and being aware of any potential challenges, you can make an informed decision about your homebuying journey.

We can help you secure a mortgage that aligns with your financial goals and help you explore other options if shared ownership is not the right fit for you.

Whether you’re taking your first step onto the property ladder or want to help a loved one buy their home, we’re here to help.

Please note: This blog is for general information only and does not constitute financial advice, which should be based on your individual circumstances. The information is aimed at retail clients only.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.

Production

Production